International Development ISSN 1470-2320 Prizewinning Dissertation 2022

No.22-SC

Fiscal Responses to Conditional Debt Relief:

the impact of multilateral debt cancellation on

taxation patterns

Sara Cucaro

Published: Jan 2023

Department of International Development

London School of Economics and Political Science

Houghton Street Tel: +44 (020) 7955 7425/6252 Fax: +44 (020) 7955-6844

London Email: d.daley@lse.ac.uk

WC2A 2AE UK

Website: http://www.lse.ac.uk/internationalDevelopment/home.aspx

DV410 37362

ABSTRACT

The 1996 HIPC Initiative reduced the multilateral debt obligations of 37 developing countries by $76 billion, becoming the largest initiative for improving the debt sustainability of developing economies. While LICs are experiencing a renewed surge in debt obligations, understanding the impact of forgiveness on public finances is of fundamental importance. The present study performs a DiD analysis on 48 Sub-Saharan Countries estimating the impact of debt relief on the recipients’ fiscal capacity. A positive and highly significant impact of HIPC on revenues and taxation levels can be identified, potentially signalling an improvement in LICs’ fiscal policies and government finances management.

DV410 37362

Table of Contents

List of Abbreviations ……………………………………………………………………………………………………………

Introduction ……………………………………………………………………………………………………………………….

Literature Review ………………………………………………………………………………………………………………

Mechanisms, objectives and limitations of Debt Relief ………………………………………………………….

Multilateral forgiveness: HIPC & MDRI ……………………………………………………………………………

The PRSP approach to conditionality: analysis and criticism ………………………………………………..

Tax reform and fiscal sustainability in LICs ……………………………………………………………………….

Fiscal reforms and taxation policies in LICs ……………………………………………………………………….

Dataset and Methodology Description ……………………………………………………………………………….

Dataset and Sample Description ………………………………………………………………………………………..

Difference-in-Differences Methodology …………………………………………………………………………….

Limitations ……………………………………………………………………………………………………………………..

Estimated Equation ………………………………………………………………………………………………………….

Dependent Variables Description and Parallel Trends Assumption ……………………………………….

Independent Variables Description ……………………………………………………………………………………

Findings and Discussion ……………………………………………………………………………………………………

Conclusion………………………………………………………………………………………………………………………..

Appendices ……………………………………………………………………………………………………………………….

Appendix A: Glossary and Definitions ………………………………………………………………………………

Appendix B: Tables and Graphs ……………………………………………………………………………………….

Appendix C: Robustness Checks……………………………………………………………………………………….

Appendix D: Do-File ……………………………………………………………………………………………………….

Bibliography …………………………………………………………………………………………………………………….

DV410 37362

List of Abbreviations

ATT Average Treatment on the Treated

DiD (or DD) Difference-in-Differences

DSSI Debt Service Suspension Initiative

EMDEs Emerging Market and Developing Economies

GDP Gross Domestic Product

GFS Government Finance Statistics

GNI Gross National Income

GNP Gross National Product

HIPC Highly Indebted Poor Countries

IFIs International Financial Institutions

IMF International Monetary Fund

OLS Ordinary Least Squares

MDRI Multilateral Debt Relief Initiative

PV Present Value

PRSP Poverty Reduction Strategy Paper

I-PRSP Interim Poverty Reduction Strategy Paper

SC Social Contributions

SE Standard Errors

SSA Sub-Saharan Africa

VAT Value Added Tax

DV410 37362

Introduction

As a man trying to carry an elephant, Sub-Saharan countries bear an enormous burden on their shoulders, an unsustainable amount of public debt weighting more than $702 billion1 and getting heavier as years pass by and wars, pandemics and inequality keep raging. Substantial literature has been dedicated to how excessive debt burdens draw resources away from macroeconomic reforms which could make countries more stable in the long run and more capable of experiencing positive institutional change. However, less attention has been paid to how these exceptionally heavy strains impact on the daily lives of citizens, reducing social investments, and consequently making it more difficult for the most fragile to escape poverty. As Amartya Sen would explain it “development can be seen (…) as a process of expanding the real freedoms that people enjoy”2, which not only consist in income and GDP growth, but a substantial increase in their “social and economic arrangements (for example, facilities for education and health care) as well as political and civil rights”3. In other words, “poverty leads to an intolerable waste of talent” which means that it’s not only money being lost, but “not having the capability to realize one’s full potential as a human being”4.

By redirecting resources towards social investments, the reduction of poor countries’ debt burdens might substantially impact on the opportunities that their populations enjoy, leading to a more equitable and

sustainable future development. On these premises and hopes, the ambitious 1996 Highly Indebted Poor Countries (HIPC) Initiative and the 2005 Multilateral Debt Relief Initiative (MDRI) led to a drastic reduction in multilateral debt obligations for than 37 Low- and Middle-Income Countries, for a total amount of $76 billion5. Being the largest debt cancellation initiatives ever initiated by the international community, HIPC and MDRI represent an invaluable opportunity to better understand the impact of forgiveness on government intervention and finances, examining how reforms can improve the daily lives and future opportunities of populations.

Although much attention has been directed towards the impact of debt relief on expenditure and macroeconomic indicators (as GDP, FDI investments and credit ratings), little debate considered their effect on government revenues and taxation, being the main long-term drivers of institutional, financial, and economic reforms.

The present analysis aims to shed light on the relationship between tax reform and debt relief. By freeing up resources previously employed for debt service payments and conveying those funds

1World Bank (2022)

2Sen (1999), p. 1

3Ibidem

4Banerjee & Duflo (2012)

5IMF (2021)

DV410 37362

through participatory conditionality, debt forgiveness initiatives have the theoretical ambition to favour both an increase in social expenditure and macroeconomic reforms, including fiscal improvements. However, due to issues of fungibility, additionality and institutional impairments, this connection is not as straightforward as it seems. By considering a sample of 48 SSA Countries between 1980 and 2020, the present research applies a Difference-in-Differences strategy to identify the causal impact of multilateral debt reduction on government revenues, overall tax level and indirect taxation.

Quite optimistically, evidence of a positive impact of HIPC initiative participation on both revenues and overall taxation is found, signalling a constructive use of freed-up resources for long term macroeconomic reforms. Although the LICs’ creditor composition has changed over time and the role of multilateral lending has progressively given space to new private actors (as China), studying HIPC’s impact on government finances and reforms represents an invaluable insight for designing future debt relief initiatives, whose need has drastically increased during the Covid-19 pandemic and the ongoing debt surge.

Two important examples are the DSSI and the G20 Common Framework for Debt Treatment, two reactions of the international community to the extreme debt growth caused by the Covid-19 pandemic. Better understanding the impact of HIPC’s debt relief allows to analyse these two initiatives with a critical eye and to understand the differential effect of payments postponements (leading to a so-called “Delay and Repay” tendency6) versus forgiveness. As many scholars warn against the effects of delayed relief, extensive research is still needed to clarify the mechanisms through which a reduction in debt obligations might lead to improved institutions, macroeconomic stability, expenditure, and investment in public goods. A way to assess the distributional impacts of multilateral forgiveness is to examine how the participants’ taxation structure changes in response, by analysing the causal relationship between HIPC debt relief, revenue, overall and indirect taxation.

The present research aims to contribute to this academic discussion and is articulated through the following structure. A detailed literature review will provide the theoretical fundamentals to better understand the origins of LICs debt issues, with specific reference to SSA countries. An overview of multilateral debt relief initiatives along with the PRSP approach to conditionality will be provided, as well as an overview of the distributional differences between different types of tax reforms. Subsequently, a methodological section will provide an overview of the constructed dataset and the methodology employed for constructing the control and treatment groups, and for verifying the assumptions underlying the DiD strategy. Following a brief discussion of results, some conclusions and future research suggestions will be drawn.

6Cassimon & Essers (2021), p. 3

DV410 37362

Literature Review

The Covid-19 pandemic has weighed down the already prohibitive public debt burden that LICs had striven so hard to lighten over the past decades. The progress made through the Brady Plan, HIPC and MDRI was almost entirely wiped out through the so-called “fourth wave of debt”, which started in 2010 and brought the “largest, fastest, and most broad-based increase in debt in EMDEs in five decades”7. According to Kose et al. (2021), this gradual increase in both government and private obligations was further exacerbated by the ongoing pandemic, estimating that in 2020 “total global debt reached 263 percent of GDP and global government debt 99 percent of GDP, their highest levels in half a century”8. The strength of monetary and fiscal government policies has been similarly weakened, as exceptional policy measures became necessary during this period of recession.

Re conquering stabilization in government debt will therefore require a substantial effort both on the side of IFIs and LICs, an effort made increasingly arduous by “a more fragmented creditor base than in the past and a lack of transparency in debt reporting”9. Understanding the features and impact of past debt restructuring and forgiveness initiatives can substantially contribute to this debate. Although many scholars have underlined the unfeasibility of a possible “HIPC 2.0”, its importance as a reference point for future restructuring initiatives has been left undoubted by present literature10. The present literature review will therefore not only provide an overview of HIPC’s and MDRI’s structure and their impact on taxation patterns of LICs, but will also provide some insights with respect to current initiatives, including the DSSI and Common Framework for Debt Treatment. Subsequently, an in-depth analysis of LICs tax structure will be presented, along with an overview of the possible contributions that debt relief might provide towards fiscal reform in the same countries.

Mechanisms, objectives, and limitations of Debt Relief

As Cassimon and Essers (2021) carefully underline, it would be impossible to identify only one comprehensive form of debt relief, which might be large-scale or case-based, involving private creditors or multilateral institutions, with several types of strings attached. Depending on its purposes, external debt forgiveness can substantially differ, leading to a significant degree of confusion when examining its impact. A good starting point is to consider a formal and shared definition in present literature, a fundamental step to build up any statistically robust research process.

7Kose et al. (2021), p. 1

8Ibidem

9Ibidem

10 Cassimon & Essers (2021)

DV410 37362

For the purposes of this study, the interpretation of debt relief considered is that provided by Cassimon

and Essers (2021),which proceeds as follows:

“Sensu stricto, debt relief refers to any type of change in the original debt service schedule of a loan/security that leads to a reduction of its PV, where future repayments are discounted using an appropriate (usually market-based) discount rate. PV reductions can be achieved through a rescheduling of interest or principal payments over time at below-market terms; and/or partial or full cancellation of such payments; or even a cancellation of outstanding debt stocks”11.

Measuring debt obligations in present value (PV) terms is necessary both given its intertemporal characteristics and the comparability between states and creditors that this measure allows12. Another crucial step for understanding debt relief and its objectives lies in analysing its motivations. One of the most influential studies on the matter is the research carried out by Reinhart and Trebesh (2016), who analysed the long-term impact of sovereign debt restructurings and cancellations.

The authors considered two separate time spans comprising a public and a private debt crisis, being respectively the First World War (1920-1939) and the emerging market debt crises (1978-2010). The two economists conclude that forms of debt relief different from debt cancellation (including, for example, maturity extensions and reduction in interest rates) led to a “lost decade of growth”13, therefore not causing any significant improvement in the countries’ arduous financial and economic positions.

On the other hand, debt write-offs positively impacted the debtors’ international credit ratings and growth perspectives. The evidence provided by the authors reinforced the idea that a definite cancellation of sovereign debt is needed to re-establish debt sustainability14 in accordance with Krugman’s debt overhang hypothesis, which can be summarized as follows:

“the presence of an existing, „inherited” debt sufficiently large that creditors do not expect with confidence to be fully repaid”, giving creditors “an incentive to lend at an expected loss to protect their existing claims.”15

Reducing the debt burden “to one that the country can repay”16 can therefore be beneficial both for the debtor country and the international community of creditors, improving future perspectives of repayment and long-term growth.

11 Cassimon & Essers (2021), pp. 3-4

12 Ibidem

13 Reinhart & Trebesh (2016)

14 See: Appendix A

15 Krugman (1988), p. 2

16 Idem, p. II

DV410 37362

Another reasoning behind debt relief lies in the creation of fiscal space, defined as the “budgetary room that allows a government to provide resources for a desired purpose without any prejudice to the sustainability of a government’s financial position”17. By reducing the amount of government funds redirected towards repayments, debt cancellation initiatives generate higher flexibility in institutional budgetary choices, allowing for increases in social expenditure18 and extensive macroeconomic reforms. This process is expected to increase the likelihood that future debt will be repaid and that the country’s overall financial situation will improve. However, given the heterogeneity of creditors to whom a state’s external debt is owned (including international institutions as the World Bank and IMF providing multilateral debt, the bilateral obligations owned to the twenty Paris Club members, new “emerging” non-Paris Club creditors, commercial banks, etc.), debt relief possesses unequivocal public good characteristics19. In fact, given that cancelling debt obligations towards one particular creditor or group of creditors increases the chances for other commitments to be fulfilled, a straightforward free-riding problem inevitably arises20, impairing the burden-sharing objective of debt relief per se.

Concerns on this matter have been recently raised with respect to the DSSI and Common Framework for Debt Treatment regarding the participation of external and private creditors in post-pandemic relief initiatives. While private-sector participation in debt forgiveness initiatives has been highly encouraged, this led to disappointing results and has magnified the fear that non-Paris Club creditors will try to increase their individual advantages, thus decreasing the effectiveness of the initiative while minimizing their losses21.

A concluding remark about bilateral and multilateral debt forgiveness needs to be made on the concepts of fungibility and additionality, especially when connected to IMF-related conditionalities22. As will be explained in further detail, present debt relief initiatives include the obligation to undertake macroeconomic and structural reforms, along with the implementation of “prescriptive public expenditure reforms”23 in accordance with the country specific PRSP (Poverty Reduction Strategy Paper) approach to conditionality. The creation of fiscal space for these specific policy areas is not obvious as it seems, as it inevitably depends on the amount of aid remaining equal to the pre forgiveness period24. As better explained by Burnside & Fanizza (2005), “any decline in other forms of aid would offset the value of the debt relief provided by the donors, and would imply a net

17 Heller (2005), p. 3

18 Dessy & Vencatachellum (2007)

19 Cassimon & Essers (2021), p. 5

20 Ibidem

21 Bolton et al. (2021)

22 See: Appendix A

23 Tan (2007), p. 10

24 Powell & Bird (2010)

DV410 37362

worsening of the government’s fiscal position”25. Moreover, especially when the newly generated resources are allocated through tight conditionalities, a crowding-out effect might cause the government to withdrawn other funds previously allocated to those areas26. These two issues, namely additionality of aid and fungibility of funds, represent two substantial limitations that might impair the impact of debt relief initiatives both in the short and long term. Their influence must be therefore be taken into account when analysing debt relief initiatives in an intertemporal perspective.

Multilateral forgiveness: HIPC & MDRI

To better understand why both the HIPC Initiative and MDRI were deemed necessary by the international community, it is helpful to delineate the background debt situation that doomed LICs and Sub-Saharan countries in particular. As explained by Ferry et al. (2021), the origins of LICs’ disproportionate debt burdens need to be traced back to the 1960s and 70s, when concessional lending27 was introduced followed by a period of substantial deregulation, leading to a phase of uncontrolled lending without any substantial consideration of debtor characteristics and reliability28.

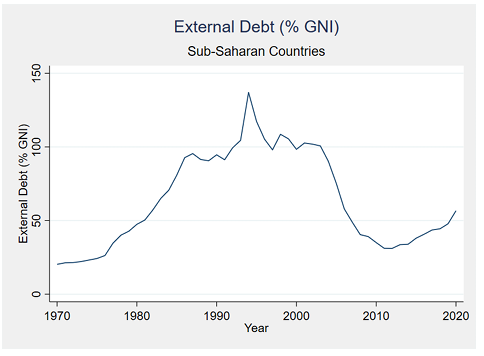

When the 1980-82 debt crisis exploded it became obvious that this process of debt stockpiling29 had become unsustainable. Drawing from Eichengreen and Hausmann’s Original Sin hypothesis30, Ferry et al. (2021) described these debt problems as exacerbated by a “double original sin”, a situation where countries “cannot usually borrow from international private sources in hard currency and subject to market conditions”31. This process can be visually observed in Figure 2.1, where both a surge in external debt (% GNI) and a decrease in 2005 (when MDRI entered in force) are displayed.

25 Burnside & Fanizza (2005), p. 14

26 Feyzioglu et al. (1998)

27 See: Appendix A

28 Ferry et al. (2021), p. 3

29 Ibidem

30 Eichengreen & Hausmann (1999), see: Appendix A

31 Ferry et al. (2021), p. 3

DV410 37362

Figure 2.1: External Debt (%GNI) of SSA, 1970-2020

Sources: World Bank’s WDI data

The responses of the international community to the rising relief requests were multifaceted, including both bilateral short-term rescheduling (Paris Club), commercial debt obligations postponement (London Club) and multilateral efforts32. These latter attempts towards multilateral relief started with the establishment of the World Bank’s International Development Association Debt Reduction Facility (IDA-DRF), with the objective of providing grants allowing particularly debt burdened countries to buy back their discounted obligations from external commercial creditors33. When this effort proved to be insufficient for adequately reducing debt obligations to sustainable levels, the World Bank and IMF jointly launched the Highly Indebted Poor Countries initiative which still remains the most extensive multilateral debt relief initiative to date designed and implemented by the international community, along with the consequent and complementary Multilateral Debt Relief Initiative (MDRI).

32 Cassimon & Essers (2021), pp. 6-7

33 Ibidem

DV410 37362

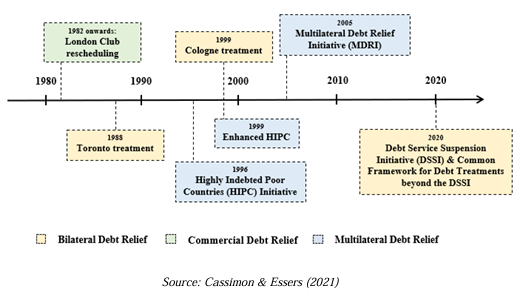

Figure 2.2: Main debt relief initiatives between 1980s and 2020

The main aim of the HIPC initiative, as stated by the IMF, is that of “ensuring that no poor country faces a debt burden it cannot manage”34. In quantitative terms, unsustainability was defined as bearing a debt service-to-exports ratio over 20-25%, as well as a stock-to-exports ratio higher than 200-250% and a debt-to-revenue ratio of more than 280%35. These thresholds defined eligibility into the initiative and were subsequently revised in 1999 to make such relief accessible to a larger number of countries in need, a reform that led HIPC to evolve into the so-called Enhanced HIPC initiative. Up to nowadays, over $76 billion in debt-service relief have been provided to 37 countries, 33 of which are located in Sub-Saharan Africa36. A further extension was provided through the Multilateral Debt Relief Initiative (MDRI), which extended its predecessor by covering the cancellation of “100% of

the claims of three multilateral institutions – the IMF, the International Development Association (IDA) of the World Bank, and the African Development Fund (AfDF) – on countries that have reach, or will eventually reach, the completion point under the enhanced Initiative for Heavily Indebted Poor Countries”37.

34 IMF (2021)

35 Cassimon & Essers (2021), p. 7. All of these thresholds are considered in PV terms.

36 IMF (2021)

37 IMF (2017)

DV410 37362

The HIPC Initiative is structured through a two-tier process, involving a decision point and a subsequent completion step. Coupled with the unsustainability requirements described above, eligible countries must be qualified to access World Bank’s IDA credit, they must have established “a track record of reform and sound policies” coupled with a first-draft Poverty Reduction Strategy Paper (PRSP) or I-PRSP38. In order to reach the decision point, eligible countries must have fulfilled these requirements and have “successfully implemented IMF and IDA-supported reform programmes for three years”39. During this period, Paris Club rescheduling under the Naples Terms and comparable treatment by commercial parties is awarded40.

If these measures prove to be insufficient for ensuring long-term debt sustainability while good performance is maintained, the participating country reaches the so-called decision point where all involved creditors define the amount of debt to be forgiven and assistance to be granted. In order to be ensured full and irrevocable debt relief, the participating country needs to follow an additional track of reforms to be defined depending on its PRSP and financial situation at the decision point. After a country-specific amount of time a “floating” completion point is reached, where substantial assistance is permanently granted41. This includes:

• Previously determined assistance, as defined after reaching the first-step decision point;

• Paris Club debt reduction up to “90% in Net PV terms”42;

• Comparable treatment granted by commercial and bilateral creditors;

• Additional topping-up and control measures by IFIs43.

However, participation of non-Paris Club and commercial creditors was largely voluntary and proved

to be insufficient, leading to “a shortfall of 8 percent of total expected HIPC assistance”44.

The PRSP approach to conditionality: analysis and criticism

A fundamental component of the HIPC initiative is conditionality, which aims to follow a bottom-up approach to development funded on country ownership of reforms through the Poverty Reduction Strategy Paper (PRSP) instrument. According to the World Bank, these can be defined as overreaching documents describing “a country’s macroeconomic, structural and social policies and programs to promote growth and reduce poverty, as well as associated external financing needs and

38 IMF (2021)

39 Cassimon & Essers (2021), p. 7

40 World Bank IEG (2006), p. 38

41 Ibidem

42 Ibidem

43 Ibidem

44 Idem, p. 34

DV410 37362

major sources of financing”45. Content development is carried out by the country itself in accordance with partners and stakeholders from the international scenario, and revised every three years46. The use of this vehicle is not limited to debt relief initiative: since its introduction, both bilateral donors and the World Bank along with the UMF facility for LICs use it as a basis for eligibility in their development programs47.

The approach behind this participatory form of conditionality can be articulated in five prepositions that constitute its foundations and main objectives. Dijkstra (2011) articulates them as follows, underlying that country-specific PRSPs should be:

(i) “country-driven, involving broad-based participation;

(ii) comprehensive, in recognition that poverty is a multidimensional phenomenon;

(iii) results-oriented, with emphasis on concrete results for the poor;

(iv) partnership-oriented, leading to better donor co-ordination under government leadership;

(v) based on a long-term perspective”48.

In compliance with these broad principles, the fiscal space generated through debt relief is directed towards social expenditure and macroeconomic reforms, including policy amendments with respect to the country’s taxation structure and redistributive arrangements. The PRSP approach has also been defined as process conditionality, as its participatory process (rather than its contents) should be assessed by donors, leading to an increased ownership of reforms and responsiveness to the citizens’ needs49.

However, much tension has been accumulated around these principles and related reforms through the years. Extensive literature, in fact, accuses this approach of neglecting truthful ownership and bottom-up participatory processes50. Many scholars including Joseph Stiglitz (2002) have pointed their finger against the PRSP instrument, which is deemed to be a revisited “one-fits-all” approach51 rather than a country-specific process conditionality52. From a financial point of view, a sharp critique has been put forward by Burnside and Fanizza (2004), according to whom this approach implies “no net improvement in the sustainability of the government’s finances”, pointing out that the inflationary impact of enhanced fiscal space and expenditure might cause “a monetary policy

45 World Bank (n.d.)

46 IMF (2016)

47 Dijkstra (2011), p. 2

48 Idem, p. 3

49 Idem, p. 4

50 Idem, p. 22

51 Stiglitz (2002), pp. 46-47

52 Dijkstra (2011), p. 113

DV410 37362

dilemma” which might lead to painful trade-offs for the government53. On a more social and institutional side, Dijkstra (2011) has pointed out how no definition of participation has been defined with respect to PRSP monitoring, making it unclear how engagement with the civil society would be ensured. These doubts, along with many others, make the debate around conditionality increasingly heated and interesting to analyse. To wrap them up in Dijkstra’s words,

“PRSPs are written because donors want them to be written, and domestic ownership of the strategies is limited. Participation processes are held because the donors want them to be held, but the elected Parliaments are barely involved, the agenda is restricted to technical issues and the participation process exercises hardly any actual influence”54.

Therefore, while on one side the PRSP approach might advance increasingly tailored poverty reduction and development strategies, its limitations still need to be taken into account as they inevitably affect the impact of debt relief initiatives on fiscal space usage (expenditure and social investments) and macroeconomic policies.

Tax reform and fiscal sustainability in LICs

According to Burgess and Stern (1993), “a healthy tax systems must be at the hearth of the public finances” for the financial sustainability of any country, making fiscal correction of essential importance to ensure macroeconomic balance in the long-term”55. To understand why this clarification is particularly important for LICs a step back is needed to the definition of Ricardian Equivalence, according to which “financing government spending out of current taxes or current deficits” has “equivalent effects on the overall economy”56, meaning that their impact on aggregate demand remains similar as rational economic agents maximize their intertemporal budget constraint over time57.

However, whether this theorem holds for LICs remains unclear and unlikely58. Although increased indebtedness might be seen as substitutable to enhanced taxation under the equivalence’s conditions, LICs need to reach a further balance between these two sources of government finance. As recently pointed out by Ofori-Abebrese and Pickson (2018), private consumption in Sub-Saharan countries tends to be positively impacted by GDP per capita and variation in interest rates, while it is negatively affected by additional “government debt, government spending, and government interest payment on the outstanding debt”59. This provides evidence for the inapplicability of this hypothesis

53 Burnside & Fanizza (2005), p. 1

54 Dijkstra (2011), p. 21

55 Burgess & Stern (1993), p. 767

56 Boyle (2020)

57 Ofori-Abebrese & Pickson (2018), p. 468

58 Burgess & Stern (1993), p. 767

59 Ofori-Abebrese & Pickson (2018), p. 466

DV410 37362

to LICs in SSA. Given this evidence, Burgess and Stern (1993) assert that a concrete substitute to taxation for sustaining long-term government expenditure in LICs is currently inexistent, making fiscal correction the basis for long-term macroeconomic stabilization. In conclusion, tax reform remains a fundamental element for a sustainable and lasting stabilization process to be established in emerging economies. As a consequence, it remains among the main objectives put forward by IFIs while jointly drafting PRSPs with countries receiving debt relief. Analysing whether these exert any effects on the amount of revenues collected and taxation rates in participating countries means not only evaluating the impact of debt relief, but also to tentatively assess whether conditionality was able to redirect fiscal space funds towards macroeconomic reforms.

Fiscal reforms and taxation policies in LICs

A brief but fundamental clarification shall be made on the composition of government revenues in LICs, and on their respective poverty and inequality impact. In the comprehensive analysis carried out by Gemmell and Morrissey (2005), it is importantly underlined that tax reforms proposed by IFIs for developing countries typically include some common elements, which comprise a reduction of trade taxes in favour of domestic sales taxes, reduction of excessively high taxation levels and progressive income tax reforms, along with a tendency towards a gradual “opening-up” of the economy and a reduction of government deficits60. Considering the distributional effects of different tax structures and reforms allows to depict their impact on inequality, an issue that has often been neglected in present literature61.

As underlined by Gemmell and Morrissey (2005), assessing these differential burdens is not an easy task, and needs scholars to make substantial assumptions regarding the statutory and economic incidence of a particular tax62. By combining several methodologies for quantifying distributional impacts of different types of taxes (namely tax progression evidence, concentration curves, tax dominance estimates, marginal social costs of taxation and CGE models), the authors reached the following conclusions regarding the burden these impose on the poor.

• Import taxes tend to be the most regressive, unless they contribute to eliminating taxes on

intermediaries (an effect that might anyways be negligible);

60 Gemmell & Morrissey (2005), p. 131

61 Idem, p. 132

62 Idem, p. 134

DV410 37362

• Export taxes need to be assessed on a case-by-case basis, as their impact inevitably depends on „the relative importance of poor producers in production of the good in question”63 and on whether there are implicit taxes;

• Similarly, also indirect taxes need to be studied depending on country- and poor-specific consumption patterns. As a rule of thumb, the authors that the taxation of goods as kerosene, which are highly consumed by the poor (for heating purposes) but not by the rich population, might be severely regressive and widen inequalities over time;

• The rationalization of excise taxes, which have traditionally been considered as regressive, could boost the country’s overall efficiency without considerably harming the poor;

• VAT represent a viable tariffs and excises replacement as it doesn’t negatively affect existing inequalities and might “assist the poor by removing serious price distortions”64;

• Income taxes are tricky to analyse in LICs, especially given to the size of their informal labour markets. According to the authors, these are likely to involve a reduction in progression dictated mostly from the fact that they were even less progressive prior to the reform65.

In conclusion, the authors underline that a change in the government revenue structure becomes inevitable as countries develop, and the taxation share in total government revenues increases over time. Although this could be seen as a gradual ongoing process caused by development processes in middle-income and emerging economies, poor developing countries experience a different situation in which the passage from trade to sales taxes is caused by a tax structure reform66. Defining the impact of enhanced fiscal space generated by debt relief on taxation patters gives therefore invaluable insights to understand how the macroeconomic reforms included in PRSPs combined with freed-up funds might impact on the poor.

Quantifying the distributional impact of debt relief through the analysis of taxation proves to be particularly needed while facing LIC’s pandemic-caused surge in debt obligations, allowing the academic community to identify those reforms and conditionality instruments that prove to be most effective in enhancing poverty-reduction and long-term economic and financial stability.

63 Idem, p. 141

64 Idem, p. 142

65 Ibidem

66 Idem, p. 142-143

DV410 37362

Dataset and Methodology Description

As previously underlined, the present analysis has the objective of assessing whether a causal relationship between the HIPC Initiative and fiscal reforms can be found. It considers a sample of 48 Sub-Saharan countries, including data for 24 participating and 24 control states over the time span 1980-2020. The present section lies the foundations for the applied DiD strategy by carefully describing the examined dataset, dependent and independent variables, the DiD methodology and its assumptions.

Dataset and Sample Description

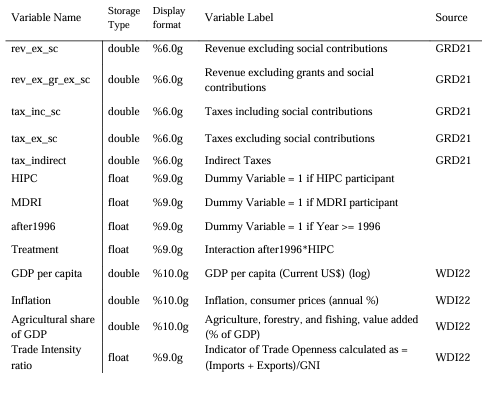

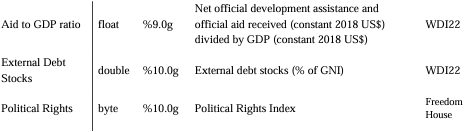

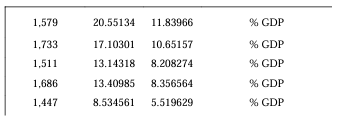

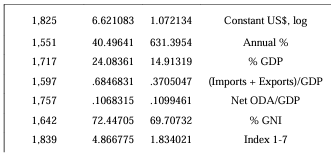

The constructed dataset has been independently assembled by the author using data from three open source databases available online, being respectively the UNU-WIDER Government Revenue Dataset (GRD), the World Bank’s World Development Indicators (WDI) and Freedom House. It is composed of 16 variables in total, including five dependent variables and seven control variables.

Table 3.1: Dataset Description

The choice to limit this analysis to Sub-Saharan Africa, as previously specified, draws from the fact that 30 over 37 post-completion point HIPC participant countries are located in this geographical area. Considering a sample of 48 countries drawn from this common location allows us to assume a degree of proximity and similarities between non-participating and HIPC countries, especially with respect to overall development and socio-economic indicators. This is essential for applying an empirically sound DiD approach, as will be explained in the next section.

The time frame considered ranges from 1980 to 2020, which allows to capture the surge in external debt experienced by Sub-Saharan countries during the 80s – according to Greene & Khan (1990), “from an estimated US$8 billion in 1970, the total external debt of African countries (excluding arrears) has risen to an estimated US$174 billion at end-1987”, amounting to “seven and a half times its level in 1970” if measured in constant 1980 US dollars67. Considering 1996 as the HIPC’s starting year, this timespan allows to consider 16 years prior to the Initiative and 24 after, allowing to convey a broad picture of the impact that debt relief has had on the explained indicators.

Difference-in-Differences Methodology

The HIPC Initiative offers an invaluable opportunity to assess the impact of multilateral debt relief on revenues and taxation patterns, in so far as it resembles a natural experiment by representing an exogenous change in government policy68 which inevitably impacts the utilizable fiscal space for a group of Sub-Saharan governments. In fact, two clusters of countries are generated: those directly affected by the treatment, whose multilateral obligations are sharply reduced, and those not taking part in the initiative and whose debt levels remain unaltered. These can be respectively defined as treatment and control groups.

67 Greene & Khan (1990), p. 1

68 Woolridge (2013), p. 457

DV410 37362

Table 3.2: Composition of Treatment and Control groups

The composition of these two groups requires an adequate explanation. It must be underlined that participation timing in the HIPC initiative is staggered as reaching its decision point depends on the country’s successful implementation of reforms and PRSP development. However, the present study considers 1996 as the treatment year for several methodological reasons:

• The process required for reaching HIPC’s decision point and interim debt relief lasts 3 years69 and involves the implementation of policies which are likely to improve the macroeconomic stability of the country in question, involving a “track record of good performance” and a PRSP or I-PRSP. Therefore, it is reasonable to consider as treatment the year in which the list of eligible countries was announced, even if these took few years for completing the mandatory eligibility steps.

• Given that the list of eligible countries was disclosed in 1996, considering this as the treatment year allows us to capture signalling effects due to this public announcement.

• The majority of countries reached their decision point around the year 2000, meaning that their eligibility process begun around 1996.

However, some countries did embark in the HIPC journey substantially later and their inclusion in the treatment group would the statistical robustness of this analysis, reason for which only those countries which participated to the Initiative prior to 2005 have been included in the Treatment group70. As a consequence, Central African Republic (2007), Comoros (2010), Republic of Congo

69 World Bank IEG (2006), p. 37

70 See participation timing table in Appendix B

DV410 37362

(2006), Cote d’Ivoire (2009), Liberia (2008), Somalia (2020) and Togo (2008) were alternatively included in the Control Group.

Given that this treatment has not been randomized71, a quasi-experimental identification strategy as Difference-in-Differences (DiD) is appropriate. This methodological choice consists in comparing the two groups over a pre-treatment and post-treatment period. By interacting a binary time variable with a treatment dummy, this strategic choice makes it possible to obtain an ATT (Average Treatment on the Treated) estimate isolating the effect of the HIPC initiative on the participant group by differencing-out the trend distance between the two considered groups. Moreover, DiD allows to account for state and year-level unobserved factors by assuming that the two groups of states would have followed similar paths in the absence of a policy variation72. This is the key identifying assumption of this methodology, defined as parallel trends or common trends assumption, according to which it should be presumed that the dependent variable’s trend and dynamics would have been the same for both groups in the absence of a treatment.

Limitations

As explained by Angrist & Pischke (2009), the DiD methodology can be seen as a “version of fixed effects estimation using aggregate data”73, which permits to identify variations in the regressor of interest that can hardly be observed at the individual level. As a consequence, DiD assumes that bias in policy evaluations must be due to state and year-level unobserved factors74, promising to deliver estimates capable of eliminating endogeneity issues arising from the comparison of essentially heterogeneous individuals75. However, many scholars have expressed doubts about DiD estimates’ reliability, raising issues linked to serial correlation and standard errors inconsistency.

This issue was specifically raised by Bertrand et al. (2003), who underline “papers that employ DD estimation use

many years of data and focus on serially correlated outcomes but ignore that the resulting standard errors are inconsistent”. The present research considers a control and treatment group drawn from the same geographical area, reason for which it’s challenging – if not impossible – to prove that regional shocks are serially uncorrelated76. Clustering standard errors at the country level – as included while presenting estimates in the Findings and Discussion section – is a forthright way to counter this

71 Cunningham (2021), p. 473

72 Ibidem

73 Angrist & Pischke (2009), p. 170

74 Idem, p. 169

75 Bertrand et al. (2003), p. 250

76 Angrist & Pischke (2009), p. 237

DV410 37362

methodological limitation. In fact, as displayed in Table 4.3, clustering SE at the country level makes

estimates for indirect taxation statistically insignificant at the 5% level77. Another fundamental limitation of the DiD design lies in the parallel trends assumption, as its validity relies fundamentally on the treatment being exogenous. This assumption is defined as conditional independence. In other words, “after conditioning on a set of observed covariates, treatment assignment is independent of potential outcomes”78. Treatment exogeneity can’t simply be verified through data analysis and has been widely criticized in present literature. Masten and Poirier (2017) identified conditional c-dependence as an alternative assumption, stating that “the probability of being treated given observed covariates and an unobserved potential outcome is not too far from the probability of being treated given just the observed covariates”. This alternative assumption represents one possible solution, among those presented in wider literature, to verifying the conditional independence assumption.

Estimated Equation

The performed Difference-in-Differences analysis is constructed through the following estimated

equation:

yi𝑡=𝛽0+𝛽1𝑎𝑓𝑡𝑒𝑟1996+𝛽2𝐻𝐼𝑃𝐶+𝛽3𝑡𝑟𝑒𝑎𝑡𝑚𝑒𝑛𝑡+𝛾𝑋𝑖𝑡+𝛿𝑖+𝜀𝑖𝑡

y𝑖𝑡 represents the eight dependent variables considered. After1996 is an autonomously constructed dummy capturing the time trend in the considered empirical setting, being equal to one subsequently to the treatment year, and zero otherwise. HIPC is the policy variable of interest separating the control and treatment groups, equal to one for countries participating in the HIPC initiative and zero otherwise. The impact of debt relief on the dependent variable of interest is captured by the interaction between the time and policy dummies, denominated as treatment. Our parameter of interest is therefore 𝛽3, allowing us to identify the estimated ATT associated with HIPC participation.

77 Although these were already weakly significant with a p-value between 0.05 and 0.10

78 Masten & Poirier (2017), p. 2

DV410 37362

Dependent Variables Description and Parallel Trends Assumption

As previously underlined, the main objective of this analysis is to provide an overview of the distributional impact of debt relief through an analysis of taxation patterns and reforms. Given that macroeconomic improvements contained in the PRSPs are country-specific, it is reasonable to examine the impact of debt relief on revenue and tax-related indicators that can provide a complete picture of a country’s taxation and redistributive pattern. The present study considers five dependent variables, listed in the following table.

Table 3.3: Dependent Variables

Variable Name Variable Label

These indicators are all derived from the UNU-WIDER GRD, which combines 58 tax-related variables for 196 countries between 1980 and 2019, providing exceptional coverage through the combination of several data sources (mainly OECD Revenue Statistics, IMF’s GFS and IMF Article IV reports)79. For ensuring adequate comparability of results, all these variables are calculated in GDP percentage. An important clarification is made by the dataset authors with respect to social contributions (SC), as these are “contributions toward a specific area of public spending”80 and therefore are not always considered alongside other taxes.

For this particular reason and for providing a more complete picture of tax patters in LICs, the present analysis considers two measures of total taxes, respectively including and excluding social contributions. In the present section a brief analysis of these selected dependent variables will be provided, as well as a verification of parallel trends for each of them. Table B.4 in Appendix B represents a basis for investigating this fundamental assumption, displaying a strong upward trend experienced by HIPC countries between Pre-1996 and post-1996 means for each dependent variable. The same trend can’t be found for control countries, which show decreasing means over time for each Regressand.

79 Oppel et al. (2021), p. 1

80 UNU-WIDER (2021), p. 3

DV410 37362

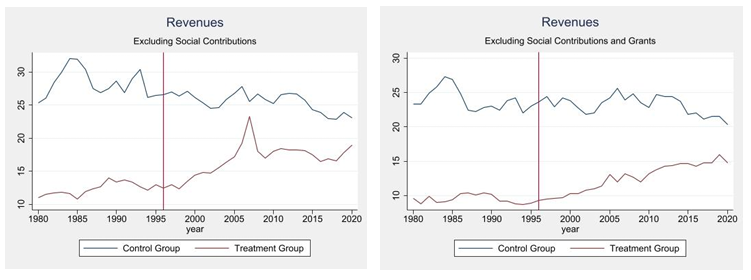

Revenue excluding SC and excluding grants and SC

Quite intuitively, taxation is ultimately needed to raise revenues, which in turn are essential for sustaining government expenditure81. Analysing the impact of debt relief and enhanced fiscal space on total revenues can therefore provide invaluable insights, as an increase in government revenues might signal an improvement in the country’s taxation policies and in the resources available finance public expenditure, including long-term support for the PRSP-related policies. The present analysis considers two measures of revenues, excluding respectively SC, and SC with grants jointly. As specified by Oppel et al. (2021), SC are intended as “compulsory and voluntary social insurance contributions from employers, employees, and the self-employed” while “grants include transfers from other government units (foreign) and international organisations”82. The exclusion of these two components is meant to consider specifically taxes and non-tax revenue components of government resources.

Figure 3.4: Revenues – Trends, Control and Treatment Group

As it can be observed through the visual inspection of the above graphs, the trends for both measures of revenues (either only excluding SC, or both SC and grants) prove to be parallel before 1996. Immediately after the treatment year, while control group countries display a slightly decreasing trend, HIPC countries clearly show a strongly growing tendency and values converging with those of non-participating countries. This analysis expects therefore to find a positive relationship between participation in HIPC and collection of revenues, possibly caused by an increase in taxation levels.

DV410 37362

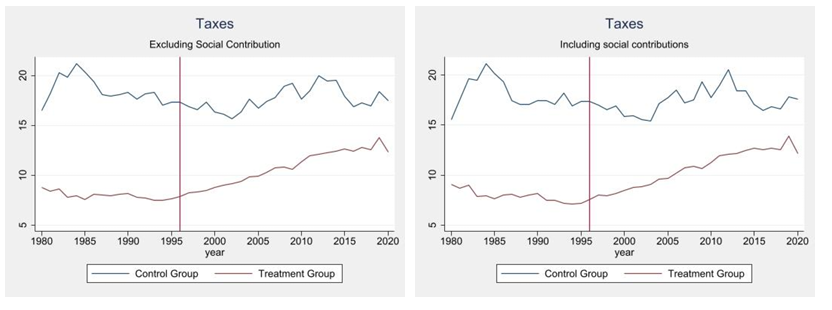

Taxes including and excluding SC

Coherently with the observed increase in revenues, the present analysis does expect to detect a related increase in taxes. This aggregate indicator captures all revenues directly derived from taxation83. Similarly to the previously observed trends, the control and treatment groups do follow a parallel path prior to 1996, subsequently to which a converging path of participating countries towards non participating ones can be observed. As a matter of fact, while taxation (as percentage of GDP) for control countries stagnates around 17-18% with a temporary increase between 2003 and 2015, taxation levels for treated countries increase from around 7-8% to 12.5%, a surge which appears to be further marked when including SC.

Figure 3.5: Taxes – Trends, Control and Treatment Group

indirect taxes

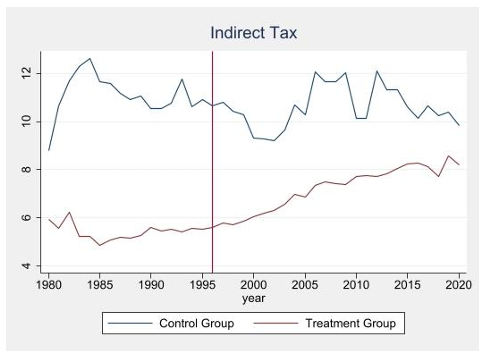

As described by Oppel et al. (2021), the considered indirect taxes measure comprises “the sum of taxes on goods and services, international trade and transactions, and other taxes”84. Although the impact of indirect taxation is difficult to assess and highly depends on consumption composition85, Gennell and Morrissey (2003) underline how these are usually not a preferred tool for redistribution, but rather easily become harmful for poor populations as they might affect some intermediate goods that are more consumed by them and more important for their daily lives. An example is that of fuel taxes which, if not excluding kerosene, might create significant regressive distortions86. Identifying a null or negative impact of debt relief on indirect taxes might therefore signal an increasingly redistributive impact, although this an essentially tentative assumption.

83 Ibidem

84 Idem, p. 6

85 Gemmell & Morrissey (2005)

86 Idem, p. 142

DV410 37362

Figure 3.6: Indirect Taxes – Trends, Control and Treatment Group

Through a quick visual inspection of trends, we do observe a that parallel tendencies were in place prior to 1996. However, after the considered treatment year the amount of indirect taxes in HIPC countries has increased substantially. Following the previously mentioned reasoning, this trend might signal a regressive rather than progressive approach to tax reform, although this highly depends on country-specific consumption patterns and specific types of indirect taxes.

DV410 37362

Independent Variables Description

Given the multiple factors that might influence government revenues and fiscal policy in developing countries, employing a simple regression methodology would be inaccurate and misleading for the purposes of this study. A deeper investigation of the factors influencing the considered dependent variables is therefore needed to perform a multiple regression analysis, which allows us to consider many factors that simultaneously impact the regressands considered87.

The model defined in this analysis controls for the simultaneous effect of seven regressors, whose choice has been made dependent on existing literature on determinants of government revenues and taxation patterns in developing countries. In accordance with the comprehensive analyses performed by Gupta (2007), Tanzi (1989) and Musgrave (1969), these are respectively GDP per capita (in log), inflation (annual %), agricultural share of GDP (% GDP), trade-intensity ratio (denominated as openness), aid-to-GDP ratio, external debt stocks (% GNI) and Freedom House’s political rights index.

87 Woolridge (2013), p. 68

DV410 37362

Per Capita GDP and Agricultural share in GDP

As underlined by Gupta (2007), per capita GDP is an indicator commonly controlled for in recent research, as it represents a proxy for the overall economic development and structural refinement of countries. It is generally expected to detect a positive relationship between per capita GDP and taxation levels. Moreover, given that some sectors are more difficult to tax than others because of their inherent characteristics, it does make sense to consider the agricultural share in GDP among the regressors. In fact, according to Addison and Levin (2012), there is an empirical negative relationship between the Tax-to-GDP ratio and the agricultural sector, especially with respect to direct taxation.

Inflation In accordance with the Optimal Taxation principle88, inflation can be used as a source of revenue by governments coping with a substantial portion of informal (or shadow) economy89. A recent World Bank policy brief drafted by Nguimkeu and Okou (2020) shows that “more than 80 percent of workers find their livelihoods in the informal sector”, numbers that have substantially increased with the COVID-19 pandemic90. Mazhar and Méon (2017) explore the relationship between informality and taxation, underlining that “a larger shadow economy should give governments an incentive to shift revenue sources from taxes to inflation, in line with the public finance motive of inflation”91, given their inability to tax a substantial portion of national incomes. Accounting for inflation when examining the relationship between debt relief and taxation is therefore important for ensuring completeness, given its balancing and substitutive role for other forms of revenue collection.

Openness

In his comprehensive literature review and analytical study, Gupta (2007) underlines how trade liberalization has exerted a substantial impact on government revenues, although ambiguous findings on this relationship have been expressed in present literature.

Leamer (1988) defines the so-called trade intensity ratio92 as the basic measure of trade openness. This is calculated by dividing the sum of imports and exports by the country’s Gross National Product (GNP). Drawing from this methodology, the present analysis includes a similar openness indicator calculated in the same way, substituting GNP with countries’ Gross National Income (GNI). This slight departure from traditional literature is due to both analytical and organizational reasons.

88 Mazhar & Méon (2017), p. 89

89 Ibidem

90 Nguimkeu & Okou (2020), p. 1

91 Mazhar & Méon (2017), p. 89

92 Leamer (1988), p. 148

DV410 37362

GNP is calculated as the “total value of final goods and services produced during a certain period (year), from inputs belonging to residents of the country, regardless of the geographical location of production”93. The main difference with the traditional Gross Domestic Product (GDP) measure is the incorporation of resident’s income gained outside of the country in question, a detail which makes this measure more representative of national economic activity.

G𝑁𝑃=𝐺𝐷𝑃+𝑁𝑅 (𝑁𝑒𝑡 𝐼𝑛𝑐𝑜𝑚𝑒 𝑓𝑟𝑜𝑚 𝑎𝑠𝑠𝑒𝑡𝑠 𝑎𝑏𝑟𝑜𝑎𝑑)

Wℎ𝑒𝑟𝑒 𝑁𝑅=𝐹𝑎𝑐𝑡𝑜𝑟 𝐼𝑛𝑐𝑜𝑚𝑒 𝑓𝑟𝑜𝑚 𝐴𝑏𝑟𝑜𝑎𝑑−𝐹𝑎𝑐𝑡𝑜𝑟 𝐼𝑛𝑐𝑜𝑚𝑒 𝑝𝑎𝑖𝑑 𝑡𝑜 𝑎𝑏𝑟𝑜𝑎𝑑94

On the other hand, GNI is defined as “gross domestic product, plus net receipts from abroad of compensation of employees, property income and net taxes less subsidies on production”(OECD, 2022). This is a very similar measure to GNP, calculated as:

G𝑁𝐼=𝐺𝑁𝑃+𝑁𝑆 (𝑁𝑒𝑡 𝑆𝑢𝑏𝑠𝑖𝑑𝑖𝑒𝑠 𝑓𝑟𝑜𝑚 𝑎𝑏𝑟𝑜𝑎𝑑)

Wℎ𝑒𝑟𝑒 𝑁𝑆=𝑆𝑢𝑏𝑠𝑖𝑑𝑖𝑒𝑠 𝑓𝑟𝑜𝑚 𝐴𝑏𝑟𝑜𝑎𝑑−𝑆𝑢𝑏𝑠𝑖𝑑𝑖𝑒𝑠 𝑝𝑎𝑖𝑑 𝑡𝑜 𝑎𝑏𝑟𝑜𝑎𝑑95

This is relevant when considering EU members, which receive subsidies from the EU and, on the other hand, fulfil customs duties obligations96. When considering Sub-Saharan countries, these two measures are equivalent. As a matter of fact, major databases including the World Bank’s World Development Indicators and OECD have permanently substituted GNP with GNI for all included countries. The trade intensity ratio considered as a control variable in the present analysis denominated as openness, is therefore calculated as follows97:

O𝑝𝑒𝑛𝑛𝑒𝑠𝑠=𝑖𝑚𝑝𝑜𝑟𝑡𝑠+𝑒𝑥𝑝𝑜𝑟𝑡𝑠

𝐺𝑁𝐼

Foreign aid

Although the direct impact of foreign aid on revenues and taxation patterns might seem unclear, its influence on fiscal space turns out to be significantly more straightforward. When assuming that debt forgiveness increases fiscal space, it is implicitly presumed that foreign aid is not crowded-out, i.e. additionality of resources98 is assumed. In other words, we need to “consider whether the countries that individually receive official debt relief also receive lower other aid flows as a consequence”99.

93 Liargovas (2014)

94 Idem; Central Statistics Office. (n.d.)

95 Ibidem

96 Ibidem

97 Data for imports, exports and GNI has been retrieved from the World Bank’s World Development Indicators and

calculated in current US$.

98 World Bank IEG (2006), p. 34

99 Bird et. al (2010), p. 220

DV410 37362

If the amount of received aid decreases when a country experiences a reduction in its debt obligations, then the participating country experiences a lower (or even null) increase in fiscal space, generating a curtailed ability to implement tax reform. Given this reasoning, we may expect the amount of foreign aid to exert a positive impact on taxation levels, given its determining role on the fiscal space generated by debt relief. However, present literature advanced ambiguous results on this matter. For example, Addison and Levin (2012) found a negative correlation between the amount of foreign aid and the tax-to-GDP ratio. It remains however a crucial determinant to be included among control variables, as also recognized by Gupta (2007) according to whom “concessional loans are associated with higher domestic revenue mobilization, while grants have the opposite affect”100. The indicator capturing this source of variability in the presented model is defined as the ratio between the country’s net official development assistance and official aid received (in current US$) scaled by

GDP (in current US$):

A𝑖𝑑=𝑁𝑒𝑡 𝑂𝐷𝐴

𝐺𝐷𝑃

External Debt

A country’s debt burden inevitably impacts taxation levels, given the necessity faced by a country to service it over time. In Tanzi (1989)’s words:

“When interest on the debt exceeds net borrowing plus the possible reduction in noninterest expenditure, the level of taxation must go up, unless the rate of growth of the economy is high enough to neutralize this increase. The size of the public debt therefore becomes a positive determinant of present and future tax levels, even though it may have been a negative influence on levels of taxation in past years”.101

A similar mechanism has been defined by Krugman in its debt overhang theory, being a situation where the debt burden is “sufficiently large that creditors do not expect with confidence to be fully repaid”, a situation which “may give creditors an incentive to lend at an expected loss to protect their existing claims”102. This mechanism eventually impacts negatively on taxation rates.

Political Rights

The relationship between institutional quality and government revenues has been extensively explored in present literature. Phuong (2015) explored a panel of 82 developing countries from 1996

100 Gupta (2007), p. 5

101 Tanzi (1989), p. 635

102 Krugman (1988), p. 2

DV410 37362

to 2013 and underlined how higher levels of corruption negatively affect tax collection in developing countries. Similarly, Brun, Chambas and Laporte (2010) found that IMF programs exert a “positive impact on public revenue mobilization”103 through the enforcement of reforms independent from political authorities.

The present analysis considers the political rights indicator defined by Freedom House as a proxy for institutional quality. Each country is assigned a rating from one to seven, where the former represents the highest degree of freedom. This index is constructed considering the country’s electoral process, political pluralism and participation, governmental functioning, and some discretionary political rights questions (including ethnic composition of governments and political balance)104.

103 Brun et al. (2010), p. 13

104 Freedom House (2018)

DV410 37362

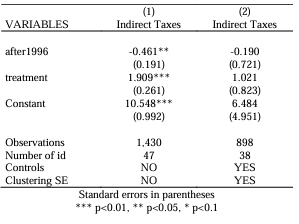

4. Findings and Discussion

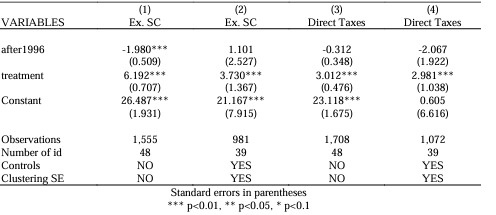

The present study finds evidence of a positive and significant effect of the HIPC Initiative on revenues and taxation rates of participating countries. In the following tables, three specifications are presented for each dependent variable: a simple regression excluding controls, a multiple regression analysis and another estimate obtained by clustering SE at the country level (hence correcting for serial correlation). The obtained results are robust to a variation in the model’s identifying assumptions and to a change of treatment year to 1999 (Enhanced HIPC). The dummy “after1996” shows the trend of each examined dependent variable over time. Since a fixed effects estimation is employed, the dummy variable “HIPC” is omitted.

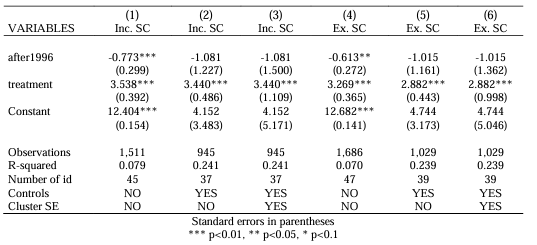

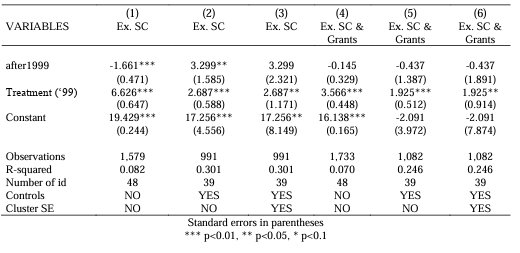

As it can be observed in the following table, revenues have been displaying a downward trend over time, which becomes slightly upward once controls are accounted for. Observing the treatment coefficient in column (3), a positive and significant impact of HIPC participation can be denoted amounting to 3.2 percentage points. The magnitude of this estimate decreases when grants are excluded along with social contributions, although the result remains significant at the 1% level. From the displayed 𝑅2 it is possible to observe that the model explains around 30% of variability in the dependent variable, signalling that other external and omitted factors are influencing the dependent variable’s trend. However, although the number of observations is drastically reduced by the introduction of control variables, the present analysis is still considering almost a thousand units.

Table 4.1: DiD Analysis – Revenues

DV410 37362

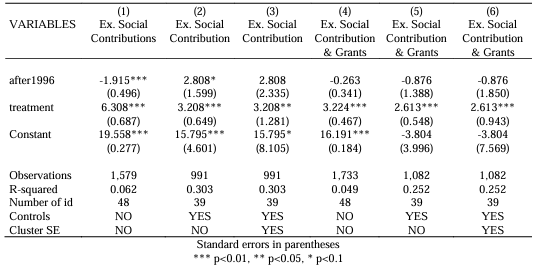

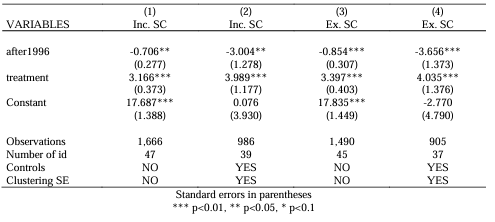

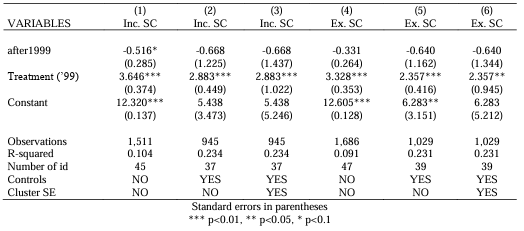

The results obtained for taxes are statistically stronger than the ones obtained with respect to revenues, and signal a positive and significant impact of participation in the HIPC initiative on the level of

taxation (both including and excluding SC) in the considered Sub-Saharan African countries. By observing the time dummy, it can be inferred that the dependent variables were experiencing a negative trend, although this is only significant when controls are excluded in (1) and (4). Considering the estimates obtained in columns (3) and (6), participation in the HIPC initiative caused an increase in taxation by 3.44 percentage points when SC are included, and 2.88 when excluded. These two results are both strongly significant at the 1% level.

Table 4.2: DiD Analysis – Taxes

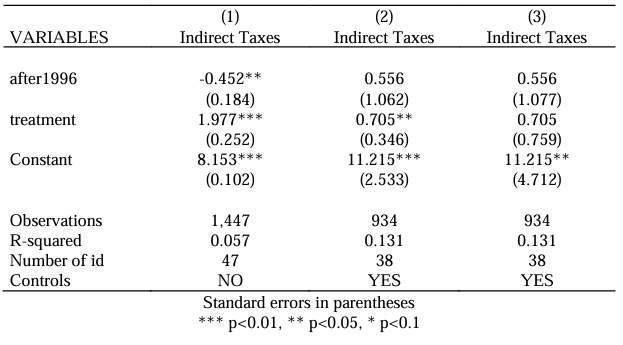

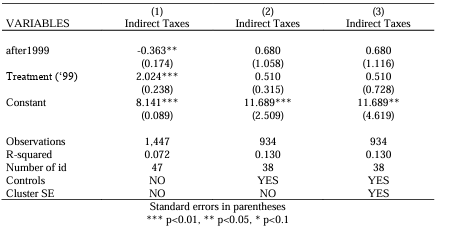

As for indirect taxes, the present analysis is unable to obtain significant evidence for the impact of debt relief initiatives. Although the result obtained in column (2) is significant at the 5% level, the estimate obtained with SE clustering signals that the previously significant value was probably due to serially correlated values. The estimate obtained in column (2) is coherent with those obtained in the table 4.2, since an overall increase in taxation levels might reasonably lead to an increase in indirect taxation too. On the other hand, this result might signal that other components of overall taxation have driven the general increase found previously. Although increases in indirect taxation have often been praised by international financial institutions, its distributional impacts on income inequality need to be carefully assessed on a country-specific basis105 – in other words, the

“redistributive scope of indirect taxes is limited and extensive rate differentiation can be problematic administratively”106, a problem that might potentially be solved designing a system of exceptions for goods whose consumption is higher among the poor107. However, as underlined by Verheul and

105 Gemmell & Morrissey (2005)

106 Burgess & Stern (1993), p. 778

107 Ibidem

DV410 37362

Rowson (2001), “most poverty reduction strategy papers ignore the complex relations between poverty and policies on trade liberalisation, tax reform, privatisation of public utilities, and cost recovery”. Therefore, a careful inspection of PRSPs remains a possible starting point for future research, possibly examining the complex relationships between different sources of tax revenue and their impact on inequality and income distribution.

Table 4.3: DiD Analysis – Indirect Taxes

Given these results, some relevant points of discussion can be drawn. Quite straightforwardly, an increase in the amount of revenues is coherent with an increase in taxation levels. These improvements, when associated with participation in the HIPC initiative, are likely to be due to PRSP related conditionalities associated with the forgiven debt. Even if these are not directly related to tax reform, the institutional improvements caused by process conditionalities might encourage tax reforms and consequent increases in revenues. Moreover, these results are coherent with findings by other authors examining the positive impact of HIPC and MDRI on public goods, especially social expenditure in education and health108. An improvement in revenue collection might give the opportunity to developing countries to invest more in public goods and infrastructural advancements109, hence improving macroeconomic conditions over time. However, as underlined by Burgess and Stern (1993), “weaknesses in the basic administrative functions of identification, assessment, enforcement, and collection often undermine the effectiveness of tax systems in developing countries”, therefore “tax reform cannot be expected to be successful unless it addresses these problems”110. A more careful inspection of post-relief taxation policies remains an interesting hint for future research.

108 Dessy & Vencatachellum (2007)

109 Bachas et al. (2021)

110 Burgess & Stern (1993), p. 820

DV410 37362

5. Conclusions

While analysing the effectiveness of tax reform in developing countries, Burgess and Stern (1993) identified a series of conditions that pushed the introduction of policy changes in the tax and redistribution realm – one of these being “a change in economic strategy involving, for example, trade liberalization, or macroeconomic stabilization”111. Although the objectives of taxation are the same in developing and developed countries – namely, to raise resources – their main difference lies “not in the objectives of government but in the constraints facing government”112. Identifying these constraints and tackling them through a realistic and tailored macroeconomic strategies remains one of the main challenges faced by developing countries and IFIs, a challenge that keeps evolving through the introduction of new instruments for imposing conditions and debates around the significance of conditionalities itself.

As demonstrated by this analysis, the HIPC Initiative has been successful in increasing revenues and taxation levels of developing countries – but how can these results be helpful for today’s worsening debt condition of many LICs, damaged by the global pandemic, global surge in inflation and energy crisis?

As recently and extensively explained by Cassimon and Essers (2021), HIPC and MDRI should now be left behind our shoulders. Although successful under many aspects, the same debt relief scheme would not lead to similar prosperous results today – especially given the major role of non-traditional lenders leading to large diversity of creditors, making it difficult to achieve consensus around large debt write-offs113. What the international community has not left behind is its “delay and repay tendency”114 in response to debt surges, a bias that risks driving developing countries towards a renewed “lost decade in development”115.

111 Idem, p. 821

112 Idem, p. 819

113 Cassimon & Essers (2021), p. 3

114 Ibidem

115 Bulow et al. (2020)

DV410 37362

Figure 5.1: LICs debt composition

As dangerously underlined by UNCTAD, “many LDCs entered the COVID-19 crisis with weaker fundamentals and greater indebtedness than they had 12 years before”116 during the so-called “third wave” of debt accumulation between 2002-9117. However, even more worrying is the response to this debt surge presented by the international community. The DSSI offered a $12.9 billion suspension of debt service repayments to 73 LICs until December 2021118, while the Common Framework for Debt Treatments introduced in November 2020 tried to provide a comparable contribution from private creditors.

Not only these proved to be insufficient for ensuring long-term (and even short- and medium-term) debt sustainability for LICs, but rewrote debates around what’s the “comparable treatment” that private lenders should concede to debt-distressed LICs119. While the international community keeps being shaken by instability, a renewed demand for new forms of debt cancellation and relief coordination arrive from LICs. Although the HIPC Initiative becomes increasingly outdated, a better understanding of its mechanisms and effects on

116 UNCTAD (2022)

117 Kose et al. (2020)

118 World Bank (2022)

119 CED (2022)

DV410 37362

macroeconomic and social stability is needed for building future solutions on solid foundations. B demonstrating the encouraging relationship between taxation improvements and debt relief, the present study underlines how future cancellation initiatives might encourage long-term macroeconomic stability of distressed countries. A renewed commitment of multilateral and private lenders must therefore be coupled with tailored forms of conditionality evolved from the PRSP approach.

As UN Secretary-General Antonio Guterres remarked, “humanitarian response, sustainable development and sustaining peace are three sides of the same triangle”120. Keeping all three together requires renewed and continuous effort towards a more equitable distribution of resources and an increasingly sustainable progress.

120 Guterres (2016)

DV410 37362

APPENDIX A – Glossary and Definitions

The present section contains several helpful definitions for better understanding the content of the present analysis. These are drawn from influential academic literature, as well as from official glossaries published by databases and IFIs.

Public Debt

For the purposes of the present study, the definition of public debt considered is the one commonly accepted by international financial institutions to enhance public debt reporting transparency. In accordance with a recent guidance published by the IMF and World Bank jointly for the compilation of Public Sector Debt Statistics (PSDS), gross public debt is defined as:

“all liabilities that are debt instruments”121 A debt instrument is defined in the same document as: “a financial claim that requires payment of interest and/or principal by the debtor to the creditor at a future date, or dates. Debt liabilities are typically established through the provision of economic value by the creditor to the debtor in exchange for a flow of future payments (principal and/or interest). These liabilities are normally under a contractual arrangement but can also be created by the force of law (such as liabilities arising from taxes, penalties, and lawsuits) and by events that require future transfer payments, such as claims on nonlife insurance companies”.122

With respect to the correct reporting of such liabilities, the mentioned financial institutions underline the following:

“Debt liabilities should be recorded when goods or assets change ownership, services are rendered, or when funds are made available. Commitments to provide funds in the future do not establish debt liabilities; amounts yet to be disbursed under a loan commitment should not be treated as debt. The definition of debt does not necessarily require that the timing of future payments of principal and/or interest is accurately known. For example, obligations of employment- related pension funds to their participants are considered debt because payments are due at some point, even though the exact timing and amount of the payment is

121 IMF (2020) p. 5-6

122 Ibidem

DV410 37362

unknown, (…) Contingent liabilities are excluded from debt liabilities because they are

obligations that only arise if a particular event occurs in the future.”.123

According to the World Bank, all those liabilities owned to non-residents must be defined as external

debt stocks124.

Additionality

The term “additionality”, in the context of this study, is linked to the substitutability or complementarity of debt relief and international aid. Powell and Bird (2010) provide the following definitions:

To define whether debt relief is additional or not, “one approach would consider whether the countries that individually receive official debt relief also receive lower other aid flows as a consequence”125.

From another point of view, debt relief might be considered additional “if it is associated with a concurrent increase in net overall resource flows from the donor-creditor concerned, or from the donor-creditor group as a whole”126.

Fungibility

The adjective “fungible” refers to the capacity of one good or service to be easily substituted to another. In mainstream literature, this notion has often been applied with reference to aid, which can be defined as fungible when “an aid-recipient country could render ear-marked aid fungible by reducing its own resources in the sector that receives aid and transferring them to other sectors of the budget”127.

A similar fungibility problem might happen when considering the PRSP approach applied by IFIs with respect to debt relief. When the created fiscal space is tied to specific social expenditure sectors and macroeconomic reforms, the government might reduce its own pre-forgiveness funds allocation to those areas, reducing the relative impact of debt relief on the targeted areas.

Conditionality

Conditionality is a fundamental component of the IMF lending and stabilization programs necessary for a country to be eligible in the HIPC initiative and MDRI. As summarized by the IMF itself:

123 Ibidem

124 World Bank (n.d.)

125 Powell & Bird (2010), p. 220

126 Ibidem

127 Feyzioglu et al. (1998), p. 30

DV410 37362

“When a country borrows from the IMF, its government agrees to adjust its economic policies to overcome the problems that led it to seek financial aid. These policy adjustments are conditions for IMF loans and serve to ensure that the country will be able to repay the IMF. This system of conditionality is designed to promote national ownership of strong and effective policies”128.

With respect to the mentioned debt relief initiative, the particular form of conditionality applied is that of PRSPs, which aim to be a participatory and bottom-up approach to the participants’ development policy.

Optimal Taxation Principle

According to this principle, “the marginal welfare cost of inflation and the marginal welfare cost of taxes should be set equal to maximize welfare”129.

Original Sin Hypothesis

As formulated by Barry Eichengreen and Ricardo Hausmann, the so-called Original Sin makes reference to a situation in which “the domestic currency cannot be used to borrow abroad or to borrow long term, even domestically. In the presence of this incompleteness, financial fragility is unavoidable because all domestic investments will have either a currency mismatch (projects that generate pesos will be financed with dollars) or a maturity mismatch (long-term projects will be financed with short-term loans)”130.

Concessional Lending

In accordance with the official definition provided by the OECD and IMF, concessional loans are those “that are extended on terms substantially more generous than market loans. The concessionality is achieved either through interest rates below those available on the market or by grace periods, or a combination of these. Concessional loans typically have long grace periods”131.

128 IMF (2021, February 22)

129 Mazhar & Méon (2017), p. 89

130 Eichengreen & Hausmann (1999), p. 3

131 IMF (2003)

DV410 37362

APPENDIX B – Tables and Graphs

Table B.1: HIPC Participation Timing

The only countries not listed in this table are Chad and Somalia. While the former reached its competion point in 2015 (becoming the 36th to receive irrevocable debt relief under the Initiative), Somalia reached its decision point in 2020.

DV410 37362

Table B.2: Independent Variables Summary Values

Revenues (ex. SC)

Revenues (ex. SC & grants)

Taxes (inc. SC)

Taxes (ex. SC)

Indirect Taxe

Observations Mean Standard Deviation Unit

Table B.3: Dependent Variables Summary Values

Observations Mean Standard Deviation Unit

GDP per capita

Inflation

Agricultural share of GDP

Openness

Aid to GDP ratio

External Debt

Political Rights

Table B.4: Pre-1996 and Post-1996 Mean Values for Treatment and Control groups

HIPC Countries Control Group

Before 1996 After 1996 Before 1996 After 1996

Revenue (ex. SC) 12.40432 16.65366 28.31331 25.51868

Revenue (ex, SC & grants) 9.494728 12.48557 23.87972 23.26643

Taxes (inl. SC) 7.856017 10.50058 18.05235 17.37329

Taxes (ex. SC) 7.935475 10.59617 18.5529 17.62938

Indirect Taxes 5.405961 7.057998 11.12907 10.58481

DV410 37362

APPENDIX C – Robustness Checks

In order to test the statistical robustness of the presented model, some robustness checks can be performed. As underlined by Angrist and Pischke (2009), modifying the identifying assumptions of a fixed effects model is particularly helpful, as mistakenly employing this methodology instead of a lagged dependent model might lead to respectively overestimation or underestimation of ATT values132.

DV410 37362

Table C.1: Revenues, Lagged Dependent Model

Table C.2: Taxes, Lagged Dependent Model

132 Angrist & Pischke (2009), pp. 183-184

DV410 37362